Florida’s Collapsing Insurance Markets

Posted: 9-7-2023 by Brent Leathwood, MBA, Licensed Florida Real Estate Broker, Cross Border Realty LLC

This blog post uses direct quotes from an article published in the Washington Post last week. Text highlighted in quotes are taken directly from the article and full credit is given to WAPO reporter Jacob Bogage.

The 800-pound gorilla in the room, that no Florida politician wants to talk about, are the collapsing insurance markets in our State.

Every month, another insurance company pulls out, or worse, leaves Floridians high and dry after a major hurricane, by declaring bankruptcy and defrauding thousands of policy holders, who have paid their premiums for years to these companies, only to be completely abandoned in their greatest hour of need.

Many of these abandoned Floridians, are elderly residents, who end up financially ruined. This is not how any senior should be forced to spend their twilight years, living in quiet desperation, defrauded out of their life savings by unscrupulous insurers.

Here are a few excerpts from Jacob Bogage’s article:

“Some of the largest US insurance companies say extreme weather has led them to end certain coverages and exclude natural disaster protections and raise premiums.”

“Major insurers say they will cut out damage caused by hurricanes, wind and hail.”

“At least 5 large US property insurers, including Allstate, American Family, Nationwide, Erie Insurance and Berkshire Hathaway, have told regulators that extreme weather patterns caused by climate change have led them to stop writing coverages in some regions, exclude protections from various weather events and raise monthly premiums and deductibles.”

“Allstate said its climate risk mitigation strategy would limit new auto and property business in areas most exposed to hurricanes.”

“Nationwide said it no longer underwrites coverage for properties within a certain distance to the coastline because of hurricane potential.”

“US insurers have disbursed $295.8 billion in natural disaster claims over the past 3 years.”

“The taxpayer backed Citizens Property Insurance in Florida was the state’s 2nd largest insurer in 2021 in terms of policies written. Fourteen insurance companies have either left Florida or have portfolios that are failing. Farmer’s, the 5th largest homeowner’s insurance provider in the US, said in July it would not renew nearly 1/3 of its policies in the Sunshine State.”

“When you see the insurance companies pulling out because the cost of rebuilding homes in Florida is bankrupting them, it’s either hubris or folly to think the state of Florida would not be bankrupted stepping in to help.”

Here is my 60 second takeaway:

1) If you are a property owner in Florida, you need to make peace with the idea, that in the very near future, you may be left to fend for yourself. Most insurance companies will have abandoned our State, and Citizens Property, the state-run insurer, may be the only option left, depending upon where your home is geographically located. And make no mistake, Citizens Property, which is funded by the State of Florida (read Florida taxpayers) does not have the financial capacity to pay out $60 billion in damages from a single hurricane event like Ian.

2) If you cannot get hurricane insurance on your home, it cannot be mortgaged. Lenders require hurricane insurance, in order to lend, against any property in Florida, they are taking as collateral for a loan. This is no minor detail and will have a very negative effect on Florida home prices. If this chain of events unfolds, inability to buy hurricane insurance, inability to get a home loan, an economic death spiral will begin, and will not be reversable.

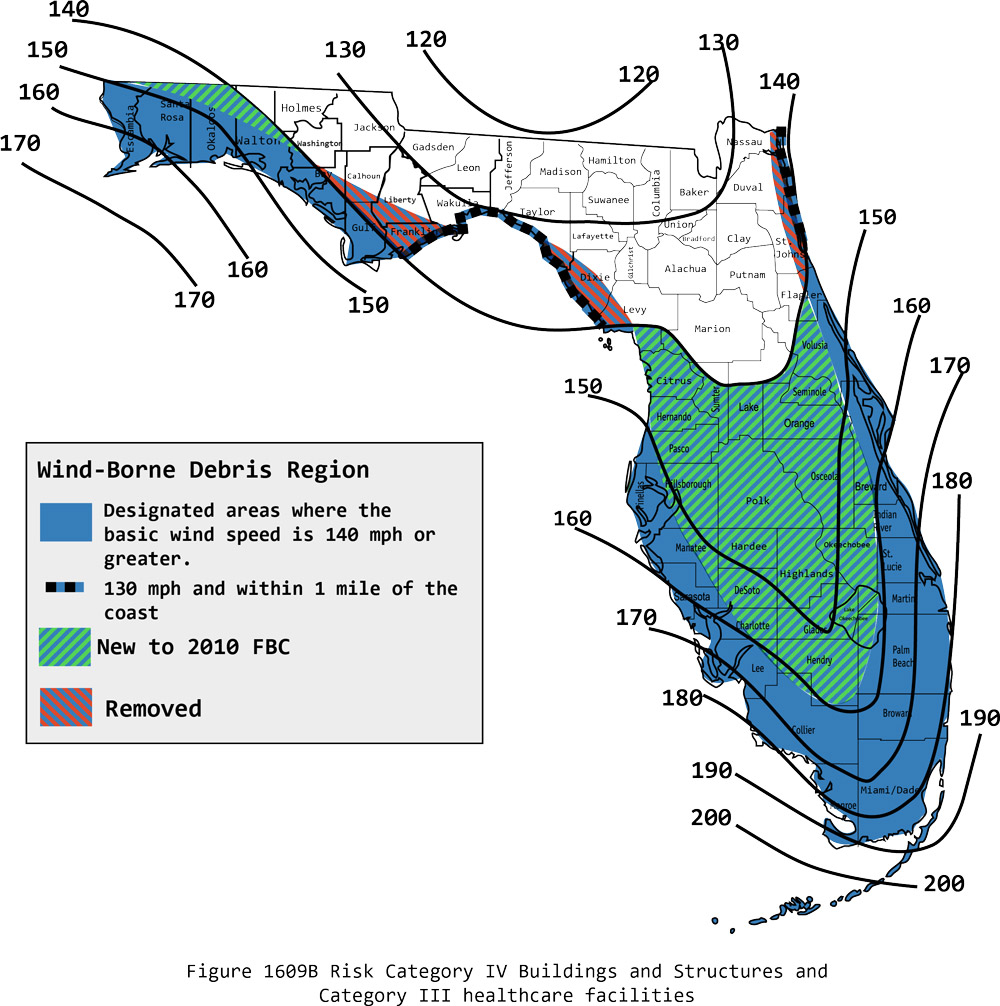

3) From a practical point of view, the “wind-borne debris region map”, which in the past provided a broad measure of risk, now needs to be combined with your local County “evacuation zone map”, showing evacuation zones in your local area. It makes sense for home buyers to seek out newer properties, not located in the earlier A-B-C-D-E evacuation zones, that are located inland, away from the coastline, that insurers consider most vulnerable to wind and flood damage.

(In Manatee County where I live, building codes for homes built prior to 2002 were designed to withstand 110 mph wind speeds, from 2002 to 2012: 130 mph wind speeds, and after 2012: built to withstand 150 mph wind speeds. In Manatee County, zone A is ordered to evacuate when potential storm surge will exceed 11 feet. Zone B 14 feet. Zone C 18 feet. Zone D 27 feet. Zone E 33 feet. My home was built in 2016, is located 20 miles inland, in Zone E. I am hoping to dodge the bullet, because my home is 35 feet above sea level, 20 miles from the coast, and built to withstand 150 mph wind speeds. But this is not a certainty.)

In 2021, during the latest Florida building code update, we saw a dramatic increase in the wind speed values shown on the wind-borne debris region map. The map now cotains 200 mph zones. See photo below. 200 mph wind speeds, are something most construction professionals, never imagined possible. To state the obvious, nothing will survive a direct hit from a 200-mph hurricane.

4) As Floridians, we need to demand our elected officials, start doing the job, we elect them to do. Which is to preserve and protect, our way of life in the Sunshine State. If they fail to act, the paradise we call home, could soon become a very different place. Hoping the next big hurricane won’t hit your area, is a fool’s errand. It is only a matter of time, until we are all impacted by these extreme weather events, either directly or indirectly.

If you live in Sarasota, and your insurance company ceases operations, because of multi-billion dollar losses they suffered on policies in Ft. Myers, that was wiped out by Ian last year, make no mistake, you will feel the pain.

We need to set aside our differences, and demand our elected officials, work together to find solutions to the challenges we all face as Floridians. Florida is an amazing place to call home, and we are very fortunate, to live in the Sunshine State.